For Healthcare executives, investors, policymakers, insurers, and technology leaders. Provided by CleverDev Software

Artificial intelligence is rapidly becoming a foundational capability across healthcare delivery, driven by workforce shortages, rising administrative burden, increasing demand for care, and sustained pressure on operating margins. According to McKinsey, generative AI could unlock between $60 billion and $110 billion annually in productivity improvements across healthcare. Morgan Stanley estimates that AI-driven efficiencies could contribute trillions of dollars in cumulative healthcare savings globally by 2050. Venture investment also continues to accelerate, with digital health and healthcare AI companies attracting nearly $4 billion in funding during recent market cycles.

This report was conducted by CleverDev Software to examine how AI adoption is reshaping clinical operations, healthcare economics, workforce structures, and enterprise strategy across providers, payers, and healthcare technology markets.

The sector is transitioning from experimentation toward disciplined enterprise implementation. Health systems, insurers, and technology vendors are increasingly embedding AI directly into operational and clinical workflows rather than deploying isolated pilot programs. Organizations positioned for long-term advantage are prioritizing interoperability, governance maturity, workforce readiness, cybersecurity resilience, and measurable operational outcomes.

The highest near-term value is emerging in administrative automation, clinical documentation, revenue cycle optimization, imaging workflows, predictive analytics, and AI-assisted clinical decision support. Radiology and pathology remain among the most mature clinical AI domains, while generative AI adoption is accelerating in ambient documentation, summarization, care coordination, and workflow orchestration systems. Industry estimates project the global AI healthcare market could exceed $180 billion by 2030 as deployment expands across enterprise healthcare infrastructure.

Predictive analytics and preventive care models are also gaining strategic importance. Large-scale AI-enabled monitoring initiatives have reported reductions of up to 79 percent in emergency visits and hospitalizations among monitored populations, reinforcing the economic value of earlier intervention and longitudinal risk management. Across healthcare systems, AI is increasingly viewed as a workforce augmentation layer that expands clinician capacity rather than replacing clinical labor.

At the same time, healthcare AI scaling remains constrained by fragmented data environments, workflow integration complexity, governance immaturity, cybersecurity exposure, model bias concerns, and clinician trust challenges. Regulatory expectations are evolving toward continuous lifecycle oversight, subgroup-level validation, auditability, and post-deployment monitoring of AI-enabled clinical systems.

Industry and investment analyses consistently indicate that the largest long-term gains will come from workflow redesign, utilization reduction, operational integration, and workforce augmentation rather than standalone automation tools. Over the next decade, organizations that successfully align AI deployment with enterprise strategy, governance frameworks, and operational transformation are likely to capture disproportionate value across healthcare delivery, payer operations, and digital health infrastructure.

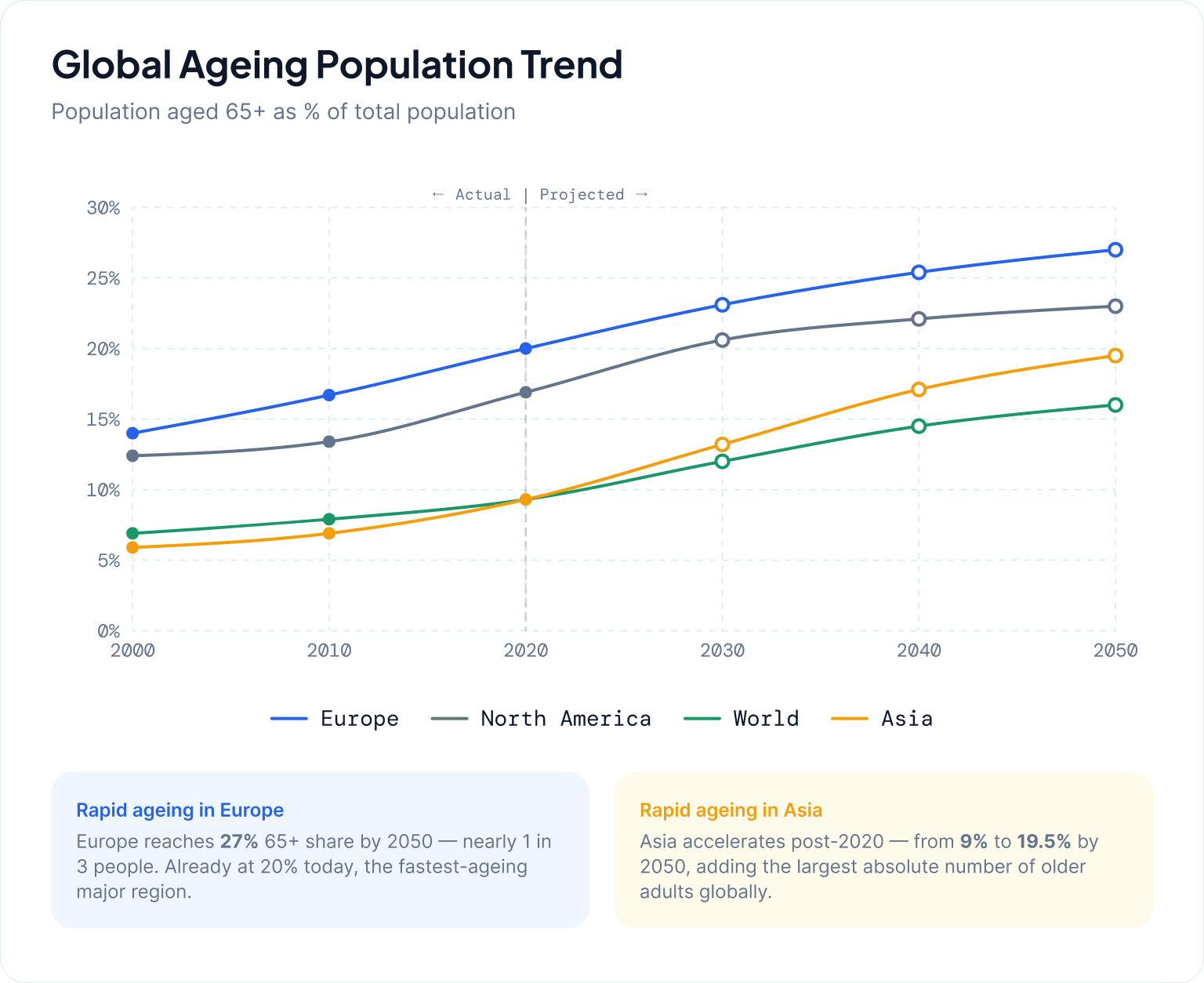

Demographic and epidemiological shifts are creating sustained structural pressure on healthcare systems globally, forming a foundational driver for AI adoption across care delivery and operations. As highlighted by the United Nations Population Fund, population ageing is accelerating worldwide, with a growing proportion of individuals living into older age brackets, fundamentally reshaping the demand profile for health and social care services. This shift is not simply extending lifespan, but increasing the proportion of people likely to experience multiple chronic conditions simultaneously, which in turn is redefining expectations for continuity and intensity of care.

This demographic transition is closely tied to a rising burden of chronic disease and multimorbidity. Health systems are increasingly managing patients with long-term, complex conditions that require continuous monitoring, coordinated care, and frequent clinical engagement. Rather than episodic treatment, care delivery is becoming longitudinal and resource-intensive, amplifying demand across primary care, specialty services, diagnostics, and post-acute care settings.

At the same time, healthcare utilization is expanding faster than system capacity in many markets. The Deloitte 2025 global healthcare executive outlook underscores that healthcare leaders are already experiencing persistent pressure from rising demand and operational strain, with capacity constraints and workforce limitations emerging as recurring challenges.

Key pressure points include:

These dynamics are compounding at a time when health systems are also expected to deliver higher-quality, more coordinated, and more personalized care. The result is a widening gap between clinical and operational demand and the ability of traditional delivery models to respond efficiently. Administrative complexity, care fragmentation, and clinician workload intensification further exacerbate system inefficiencies, limiting scalability without new forms of support.

Taken together, demographic ageing, increasing chronic disease prevalence, and sustained utilization growth are redefining baseline expectations for healthcare systems. These pressures are not cyclical but structural, suggesting that incremental efficiency improvements will be insufficient on their own. Instead, they establish the underlying rationale for AI-enabled approaches that can help extend capacity, support clinical decision-making, and streamline care delivery workflows in increasingly constrained environments.

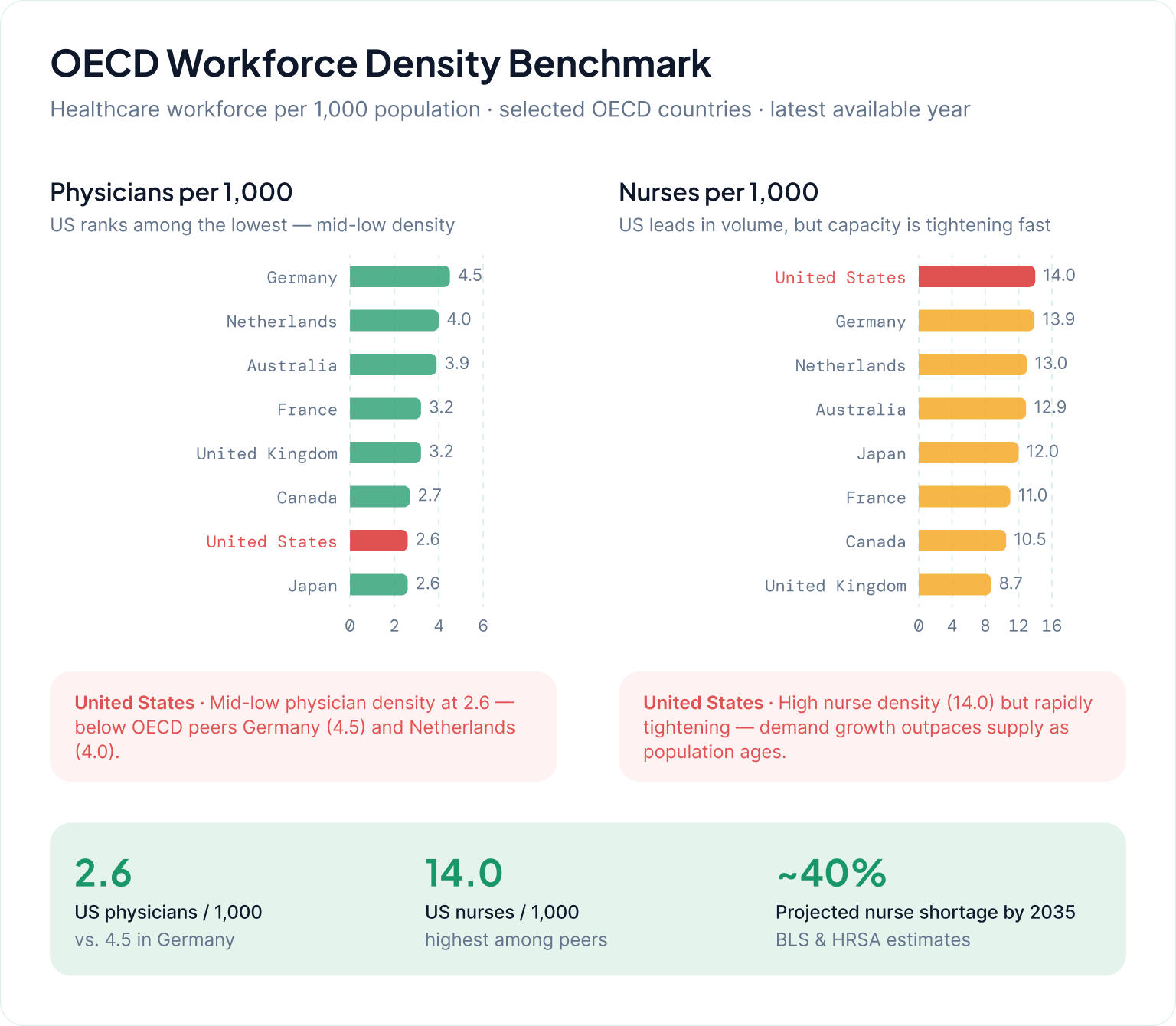

Workforce shortages and burnout are emerging as binding constraints on healthcare delivery capacity, shaping both near-term operational strain and long-term system design priorities. Across the United States, the Bureau of Health Workforce highlights sustained and widening gaps between clinician supply and demand, particularly across primary care, nursing, and several specialty areas.

At the same time, labor market analysis underscores that healthcare systems are entering a period where demand growth is outpacing workforce expansion. McKinsey’s analysis of healthcare labor markets describes a “critical shortfall” in healthcare workers, driven by ageing populations, rising care complexity, and constrained training throughput. The result is not only fewer available clinicians per patient, but also increasing reliance on extended hours, task shifting, and non-ideal staffing configurations to maintain service levels.

These structural shortages are compounded by high levels of clinician burnout, which further reduces effective workforce capacity. Survey-based evidence from the American Medical Association shows persistent strain in physician practice environments, with burnout closely tied to administrative burden, documentation demands, and inefficiencies in clinical workflows. Importantly, burnout is not only an individual wellbeing issue — it functions as a system-level capacity constraint by increasing attrition risk, reducing clinical time availability, and accelerating early retirement decisions.

Together, these forces create a reinforcing cycle: shortages increase workload intensity, workload intensity drives burnout, and burnout further reduces effective supply. From a labor economics perspective, this shifts healthcare systems away from marginal efficiency optimization and toward substitution strategies—where automation and augmentation become necessary to stabilize throughput rather than simply improve productivity.

Key structural drivers behind the constraint:

From an operating model perspective, capacity is increasingly determined by effective clinical time, not headcount alone, as burnout reduces usable labor supply even when staffing levels appear stable.

Labor scarcity is structurally persistent, shifting AI from a productivity enhancement tool to a core mechanism for maintaining service continuity under constrained workforce conditions.

Healthcare systems are entering a phase where AI adoption is no longer framed as innovation strategy, but as operational necessity driven by structural pressure. Across both payer and provider environments, the underlying economics of care delivery are being reshaped by persistent margin compression, workforce constraints, rising administrative complexity, and sustained growth in patient demand and clinical acuity.

This shift is reflected in industry analysis such as the KPMG Intelligent Healthcare Report, which characterizes AI as a foundational enabler for more adaptive, data-driven healthcare systems. Similarly, HIMSS emphasizes that AI is moving from isolated use cases into core workflow transformation across clinical, operational, and administrative domains https://www.himss.org/resources.

Operational pressure from staffing shortages and administrative burden increases the cost of manual coordination and documentation, making automation and decision support economically attractive. Financial pressure from reimbursement constraints and rising input costs compress margins. Clinical complexity from ageing populations and multimorbidity increases care coordination demands. Data saturation from exponential growth in health data exceeds human interpretive capacity, creating reliance on algorithmic triage and prioritization.

Within this framework, AI adoption is best understood as a response to diminishing marginal returns from traditional operational improvements. Incremental process optimization alone cannot close the gap between demand growth and system capacity.

As these pressures compound, AI is shifting from point solutions (e.g., imaging support or documentation tools) toward embedded infrastructure that underpins scheduling, revenue cycle management, clinical decision support, and population health management.

For healthcare leaders, the strategic implication is that AI is becoming inseparable from core operating model design. Organizations that delay adoption are not simply forgoing efficiency gains; they risk widening structural gaps in cost position, workforce sustainability, and care delivery scalability relative to more digitally mature peers.

The healthcare AI market is in a phase of sustained structural expansion, driven by both digital transformation in health systems and accelerating clinical and administrative use cases. Across major market research firms, including MarketsandMarkets, Grand View Research, and Fortune Business Insights, the consensus view is consistent: strong multi-year growth across imaging, diagnostics, workflow automation, and drug development.

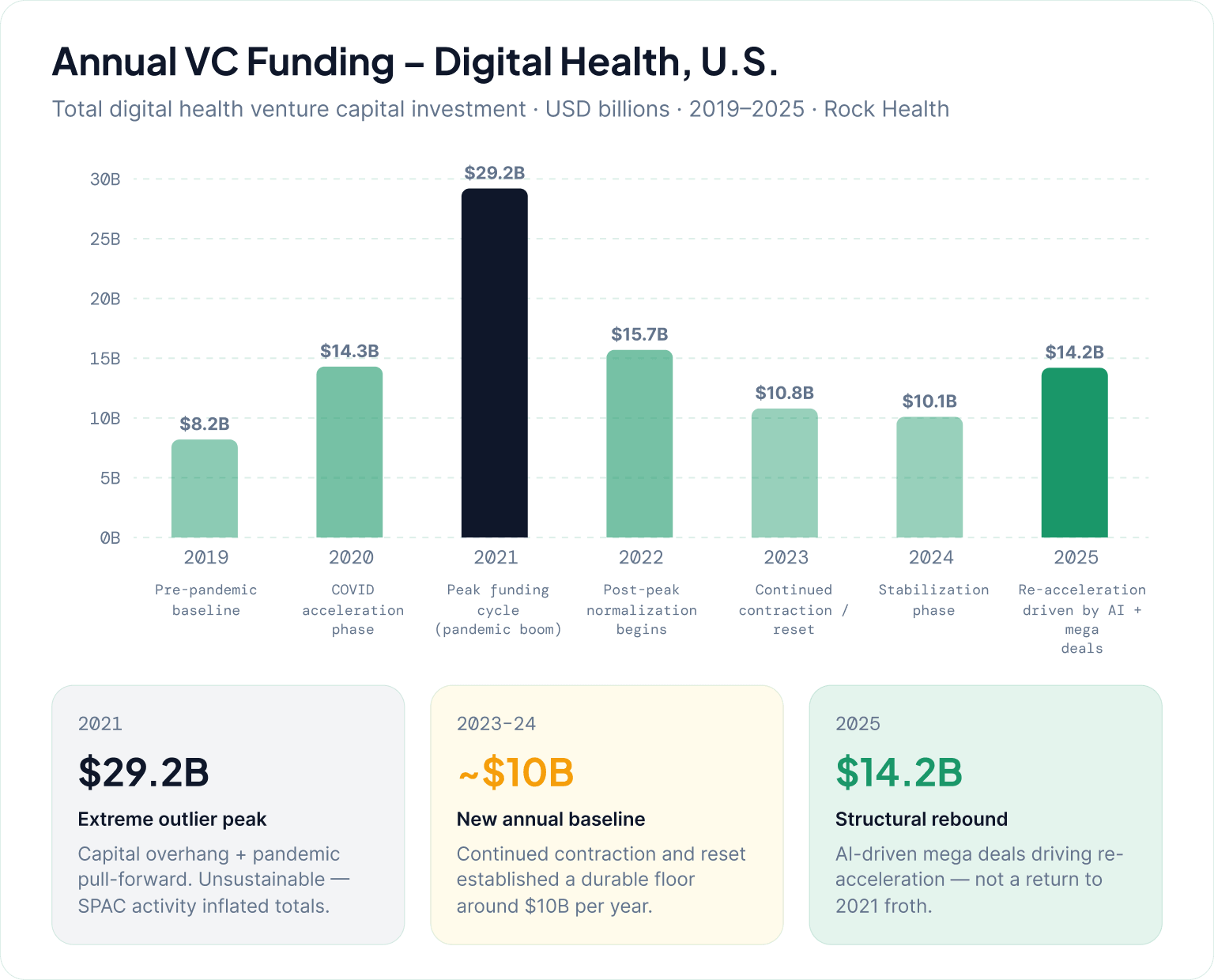

On the investment side, healthcare AI attracted nearly $4B in venture capital funding in 2025, underscoring sustained investor conviction despite broader market normalization. At the same time, Rock Health’s analysis highlights a “proof-in-the-pudding” phase where capital is increasingly concentrated in companies demonstrating measurable clinical or financial ROI.

Across segments, investment is clustering around:

Importantly, capital allocation is increasingly tied to demonstrable ROI rather than early-stage experimentation. Vendors with deep workflow integration are outperforming standalone AI tools in both funding and adoption trajectories.

A “winners concentrate” dynamic is emerging, where fewer integrated platforms capture a larger share of deployment and investment activity.

The healthcare AI competitive landscape is rapidly consolidating into a layered ecosystem where value is increasingly determined by distribution access, workflow integration, and ability to operationalize AI across clinical and administrative environments.

At the infrastructure layer sit large technology platforms including NVIDIA , Microsoft , Google, and Amazon. NVIDIA in particular has positioned itself as a foundational compute and deployment layer for healthcare AI systems.

AI-native startups remain the primary source of application-layer innovation, particularly in documentation, ambient intelligence, imaging augmentation, and administrative automation. At the same time, demand is growing for custom AI healthcare solutions designed around the operational realities of specific providers, specialties, and patient populations, enabling organizations to move beyond one-size-fits-all implementations. However, their long-term positioning increasingly depends on integration partnerships rather than standalone differentiation.

Electronic Health Record vendors remain one of the most strategically important control points in the ecosystem due to their embedded position in clinical workflows, particularly for documentation, decision support, and revenue cycle automation.

Pharma partnerships represent a distinct but rapidly expanding axis of the ecosystem. AI is being embedded into drug discovery and clinical trial optimization pipelines, with increasing emphasis on co-development models rather than traditional procurement relationships.

Health systems are increasingly acting as co-development and validation environments rather than passive buyers, with adoption patterns varying significantly by institutional maturity.

Overall, the ecosystem is converging toward integrated platforms where value accrues to entities that combine infrastructure control, workflow integration, and measurable operational outcomes.

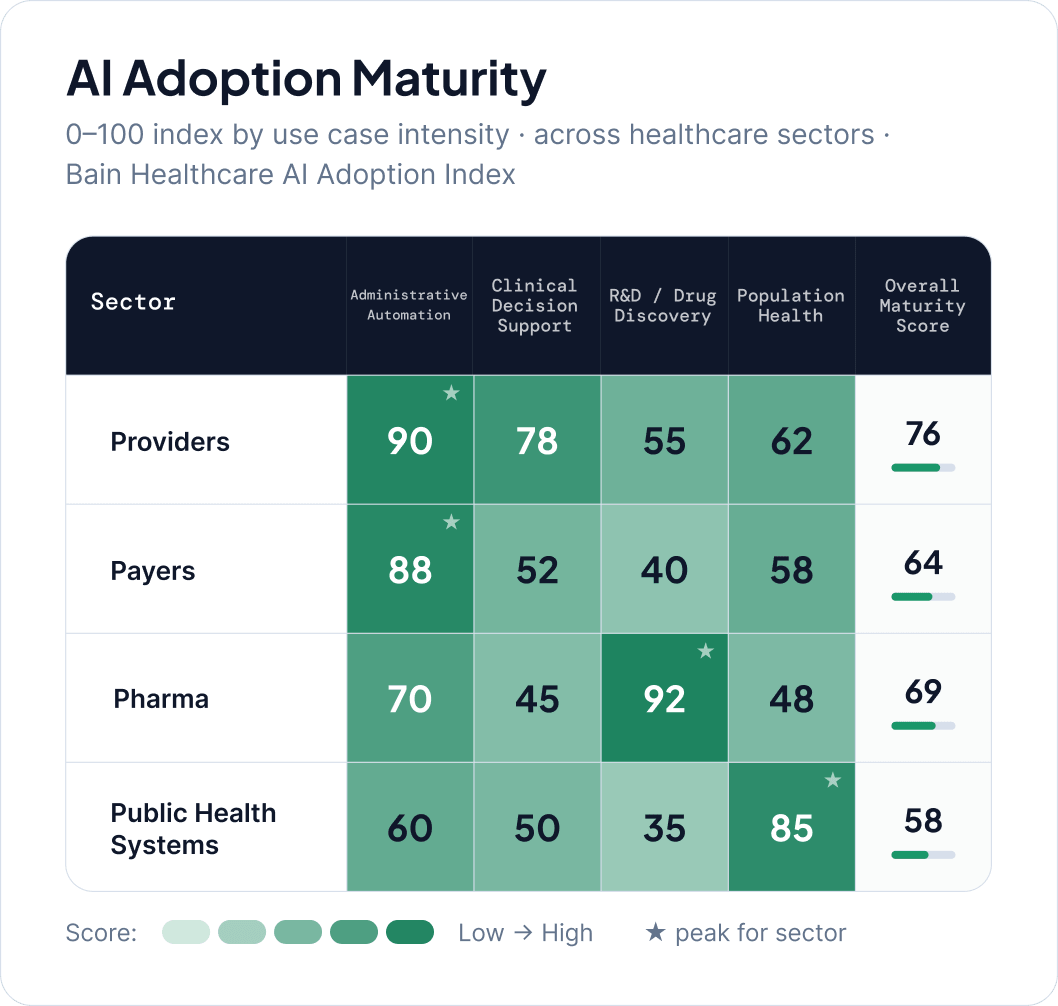

Adoption of AI in healthcare is increasingly uneven across geographies and sectors, reflecting differences in regulatory environments, infrastructure maturity, workforce readiness, and institutional incentives.

North America leads in enterprise-scale deployment, driven by system consolidation, private-sector investment, and advanced data infrastructure. Europe shows more measured adoption due to stricter regulatory frameworks and data governance requirements. Asia-Pacific demonstrates more heterogeneous but often faster scaling, particularly in national digital health programs.

Sector-level adoption patterns are similarly differentiated. Providers are the most active adopters, prioritizing administrative automation and clinical augmentation. Payers focus on claims automation, fraud detection, and utilization management. Pharma organizations emphasize drug discovery, clinical trial optimization, and real-world evidence generation. Public health systems adopt AI selectively, often centered on surveillance, outbreak prediction, and resource allocation.

Across all sectors, AI adoption typically begins with operational efficiency use cases before expanding into higher-risk clinical and system-level applications as governance frameworks mature.

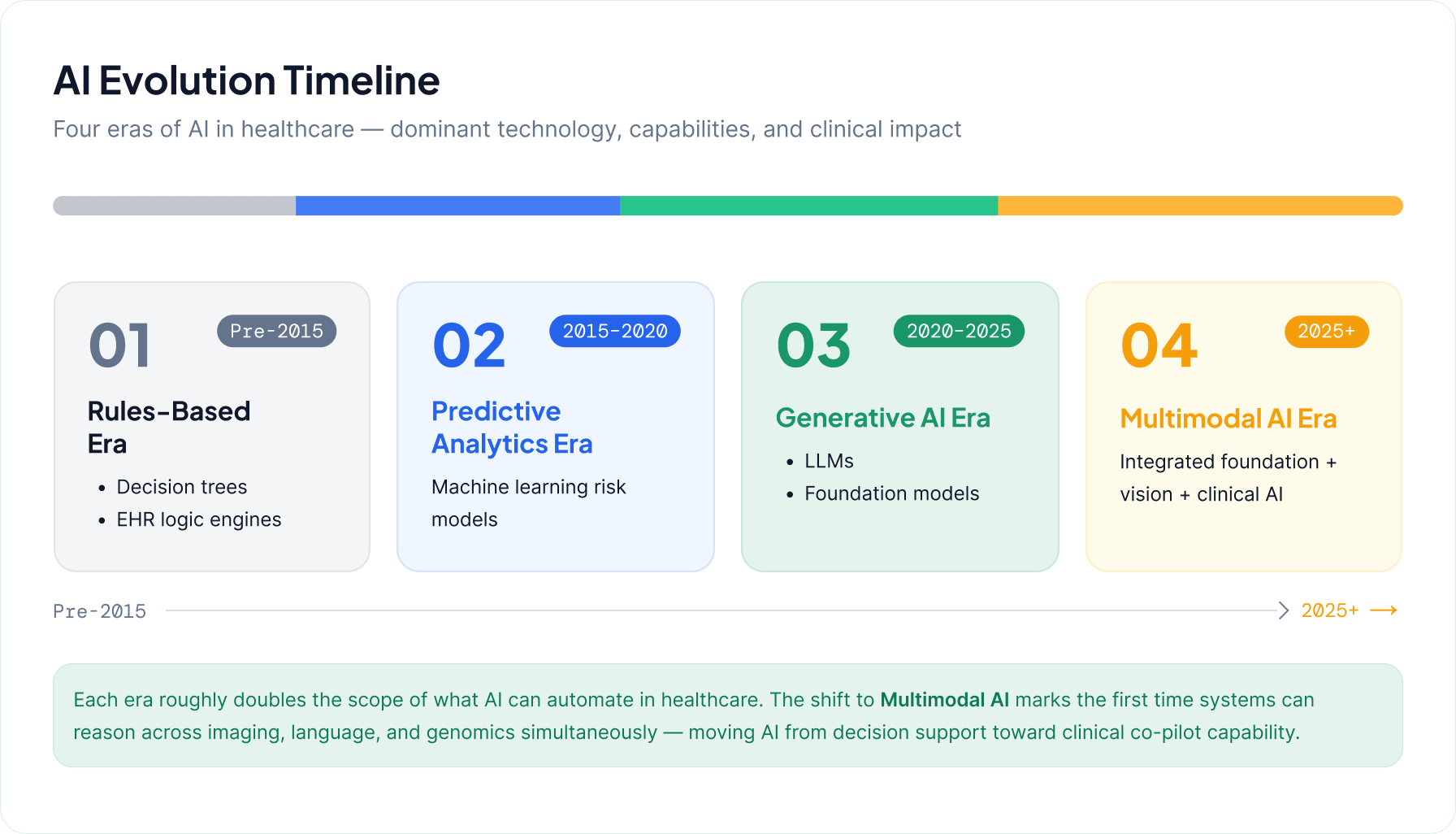

The shift from rules-based and predictive analytics systems toward large language models and multimodal AI represents a structural change in healthcare computing.

Earlier systems focused on constrained use cases such as risk scoring, readmission prediction, and protocol-based alerts. These systems improved consistency but were limited by dependence on structured data and lack of adaptability to unstructured clinical information.

Generative AI introduces the ability to synthesize clinical text, support documentation workflows, and enable more natural interaction with healthcare systems. McKinsey highlights its role in improving clinical documentation and workflow efficiency.

KPMG further emphasizes that organizations are moving toward integrated AI systems embedded across enterprise workflows rather than isolated predictive models.

Multimodal AI extends capability across clinical text, imaging, laboratory data, and voice inputs, enabling end-to-end workflow support from triage through care coordination.

Healthcare AI is evolving across three overlapping stages: rules-based systems, predictive analytics, and generative or multimodal systems. These coexist in hybrid environments rather than replacing one another.

Healthcare AI spans multiple interlocking categories embedded across clinical, operational, and research workflows.

Diagnostic AI supports imaging and pathology workflows, increasingly shifting toward augmentation and prioritization rather than standalone detection.

Clinical decision support systems combine patient data, guidelines, and predictive models to support diagnosis and treatment decisions, though adoption is constrained by explainability and integration complexity.

Ambient documentation systems reduce administrative burden by capturing and structuring clinical encounters https://www.himss.org/resources.

Predictive analytics remains foundational for risk stratification, utilization forecasting, and population health segmentation.

Workflow automation focuses on administrative processes including scheduling, claims processing, and prior authorization.

Drug discovery AI accelerates pharmaceutical R&D through target identification, molecular design, and clinical trial optimization.

Conversational AI supports patient engagement, triage, and administrative interaction, evolving from rule-based systems to context-aware models.

Agentic AI represents an emerging category capable of executing multi-step workflows across healthcare systems, though deployment remains early.

Scaled AI deployment depends primarily on infrastructure readiness rather than algorithmic capability.

Data quality remains the most fundamental constraint, with fragmentation and inconsistency limiting reliability of AI outputs.

Interoperability determines whether AI can function across systems or remains confined to isolated workflows.

Cloud infrastructure has become the default backbone for scalable deployment due to its support for elastic compute and integration.

Compute requirements are increasing significantly with generative and multimodal systems, introducing new cost and performance constraints.

Governance architecture is emerging as a central requirement, supporting monitoring, validation, accountability, and lifecycle management of deployed models.

Together, these domains define enterprise AI readiness in healthcare, determining whether organizations can move from pilot deployment to system-wide integration.

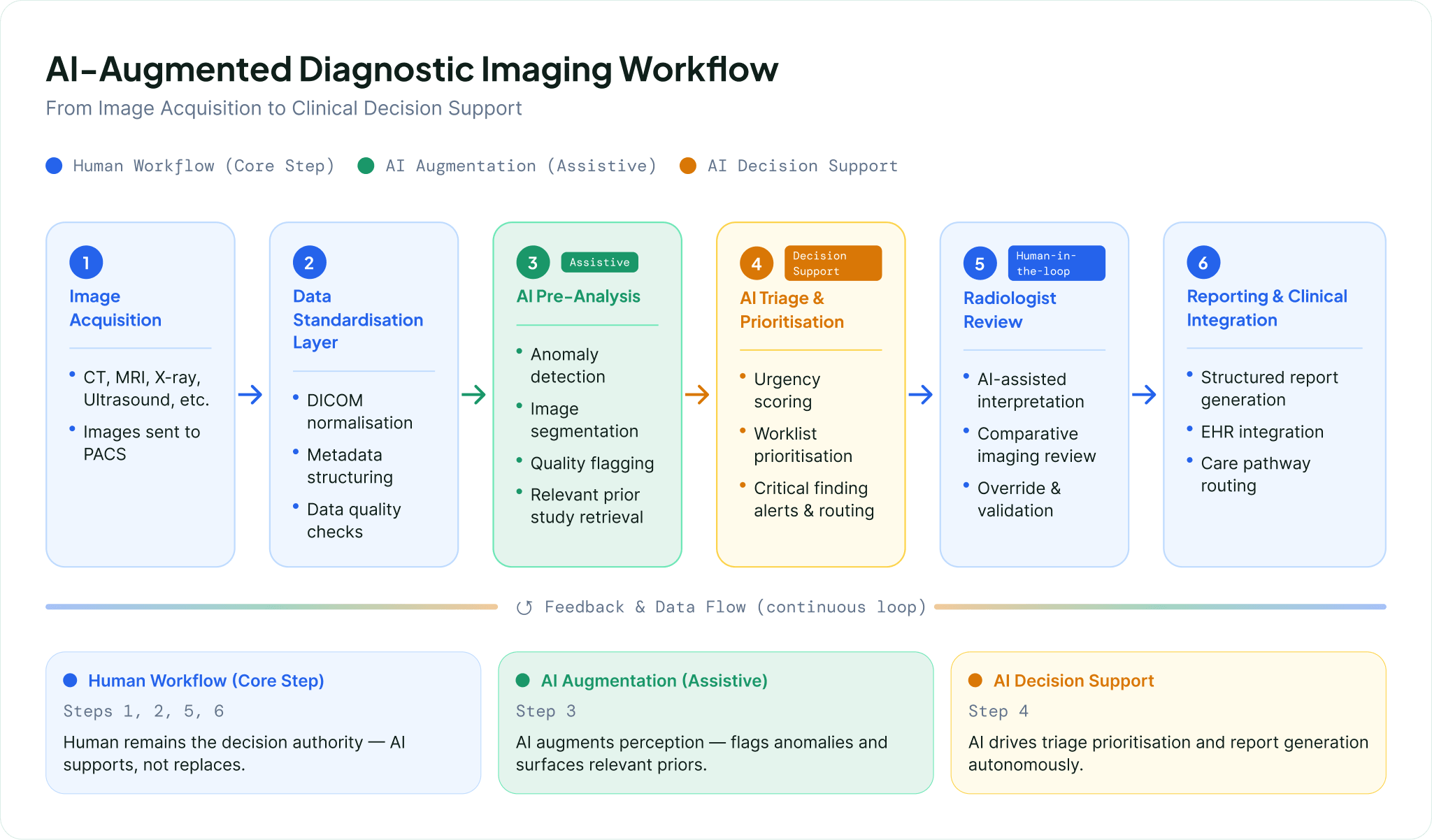

AI is reshaping diagnostics and medical imaging, with radiology and pathology representing the most mature and operationally integrated domains of clinical AI adoption. Across regulatory and industry perspectives, including the FDA framework for AI-enabled medical devices, AI is positioned as augmenting diagnostic specialists rather than replacing them, supporting earlier disease detection, improved triage, and more efficient management of growing imaging volumes Guardian AI Radiology Workforce Feature.

In radiology, AI is primarily deployed as decision support and triage tooling for CT, MRI, and X-ray interpretation. These systems flag anomalies, prioritize urgent cases, and reduce diagnostic latency in high-volume environments. AI is embedded within imaging workflows as a parallel analytical layer, allowing radiologists to focus on complex or ambiguous cases while routine detections are pre-processed.

Pathology is undergoing a similar transition through digitization of tissue samples and application of AI to whole-slide imaging. AI supports identification of cellular abnormalities, biomarker quantification, and more standardized interpretation in areas previously subject to inter-observer variability. This is particularly relevant in oncology, where diagnostic precision directly influences treatment pathways. Adoption depends heavily on digital infrastructure maturity and access to high-quality digitized datasets.

Early disease detection is a key application area, where AI identifies subtle imaging or clinical patterns that precede overt clinical presentation. This is especially relevant in conditions such as cancer and cardiovascular disease where earlier intervention significantly affects outcomes. Regulatory frameworks for AI-enabled medical devices reflect this growing clinical importance while emphasizing validation and post-market performance monitoring.

Predictive diagnostics extends imaging beyond interpretation toward longitudinal risk assessment by integrating imaging data with clinical and historical patient information. This enables estimation of disease probability, progression risk, and potential complications, shifting diagnostics from static interpretation to continuous risk evaluation.

AI-enabled imaging workflows increasingly reorganize diagnostic pipelines around automated triage. Incoming studies are prioritized based on urgency, pre-analyzed for anomalies, and routed with decision support overlays. This reduces bottlenecks in radiology departments and improves time to diagnosis in high-throughput and emergency settings:

Across all domains, AI systems are increasingly treated as regulated medical devices requiring validation, oversight, and continuous performance monitoring rather than static software tools.

Administrative automation is one of the most immediate and high-impact applications of generative AI in healthcare, particularly in reducing non-clinical workload linked to clinician burnout and operational inefficiency. Industry analyses from McKinsey and KPMG consistently highlight documentation, scheduling, prior authorization, and revenue cycle management as the highest-value near-term domains McKinsey Generative AI in Healthcare Insights.

In clinical documentation, ambient scribing and AI-generated note systems are becoming a foundational productivity layer. These tools reduce documentation burden while improving completeness and standardization of clinical records. This improves downstream coding quality and reduces administrative rework. Documentation automation is increasingly serving as an entry point for broader AI integration into clinical workflows due to its direct connection with EHR systems and clinician interfaces.

Scheduling and care coordination are being transformed through AI systems that optimize provider availability, patient preferences, and clinical urgency. These systems aim to reduce no-shows, improve capacity utilization, and streamline patient routing across multi-site health systems. Adoption is uneven but shifting toward predictive and adaptive scheduling models.

Prior authorization remains a major administrative bottleneck. AI applications focus on automating documentation assembly, mapping clinical evidence to payer requirements, and pre-validating authorization criteria. These systems aim to reduce cycle time, denial rates, and manual intervention, with effectiveness dependent on payer standardization and interoperability between clinical and administrative systems.

Revenue cycle management represents one of the most commercially mature AI applications. AI is used across eligibility verification, coding assistance, claims scrubbing, and denial prediction. Systems are increasingly evolving into integrated optimization layers that learn from billing outcomes to improve accuracy and reduce revenue leakage. This domain is often prioritized due to its direct impact on cash flow and margin performance.

Across these domains, AI is most effective when it reduces cognitive load in high-volume, rules-driven workflows while preserving human oversight for exceptions and clinical judgment. This is driving a shift from point solutions toward workflow redesign combining technology deployment with process reengineering.

Administrative burden reduction framework:

Workflow automation ROI considerations:

Predictive and preventive care represents a major shift from reactive utilization toward earlier identification of risk and intervention. Value creation is concentrated in patient risk prediction, population health management, and remote monitoring enabling earlier clinical response.

Industry evidence indicates that AI-enabled predictive systems can significantly reduce downstream utilization when deployed effectively. A reported clinical trial of an AI diagnostic tool developed by Clare Medicals found a 79 percent reduction in emergency room visits and hospitalizations among monitored patients Clare Medicals AI Diagnostic Trial Results. While methodological details are not fully disclosed, the result reflects the central value proposition of predictive AI in preventing acute escalation through earlier intervention.

Broader projections suggest AI-enabled predictive and preventive systems could contribute to large-scale systemic impact, including estimates of over 250,000 lives saved annually and a $188 billion market opportunityby 2030. These figures are model-based and directional but reflect consensus expectations of macro-level impact.

Predictive care enables a continuous care model, shifting from episodic engagement toward ongoing monitoring and risk stratification. AI systems identify high-risk patients, prioritize outreach, and allocate care management resources to those most likely to deteriorate. Effectiveness depends on data completeness and integration into clinical workflows that support timely intervention.

Key functional domains:

The primary constraint is operational integration rather than model availability, particularly embedding predictive outputs into care pathways that enable timely clinical response rather than passive reporting.

Personalized medicine and precision healthcare are being reshaped by AI systems that integrate genomics, biomarkers, imaging, and longitudinal clinical data into individualized treatment insights. The strategic shift is toward continuous, data-driven decision support that informs both clinical care and drug development pipelines Deloitte Accelerating Drug Discovery and Development.

In genomics and biomarker analysis, AI enables interpretation of high-dimensional datasets that are difficult to analyze using traditional methods. These systems identify clinically relevant genetic variants and biomarker signatures that support risk stratification and therapy selection, particularly in oncology and rare disease contexts. The primary impact is faster translation of molecular data into clinical decision inputs.

Biomarker-driven care is becoming central to precision medicine. AI improves correlation between molecular profiles and therapeutic response, supporting more targeted interventions. Operational challenges remain in standardizing biomarker data across laboratories and integrating it into clinical workflows at the point of care.

Personalized treatment pathways combine genomic, imaging, clinical, and real-world evidence data to support therapy selection tailored to individual patient profiles. AI is increasingly positioned as an accelerator of drug discovery and development, shortening the pathway from discovery to clinical application.

AI-assisted clinical decision support integrates these data streams into clinician-facing recommendations, including treatment options, contraindications, and patient-specific risk factors. Computational infrastructure and model scalability are critical enablers of these multimodal precision care workflows.

The primary constraint is clinical integration, including interoperability across diagnostic systems, EHRs, and laboratory platforms, as well as governance frameworks ensuring validation and safe use of AI-generated recommendations.

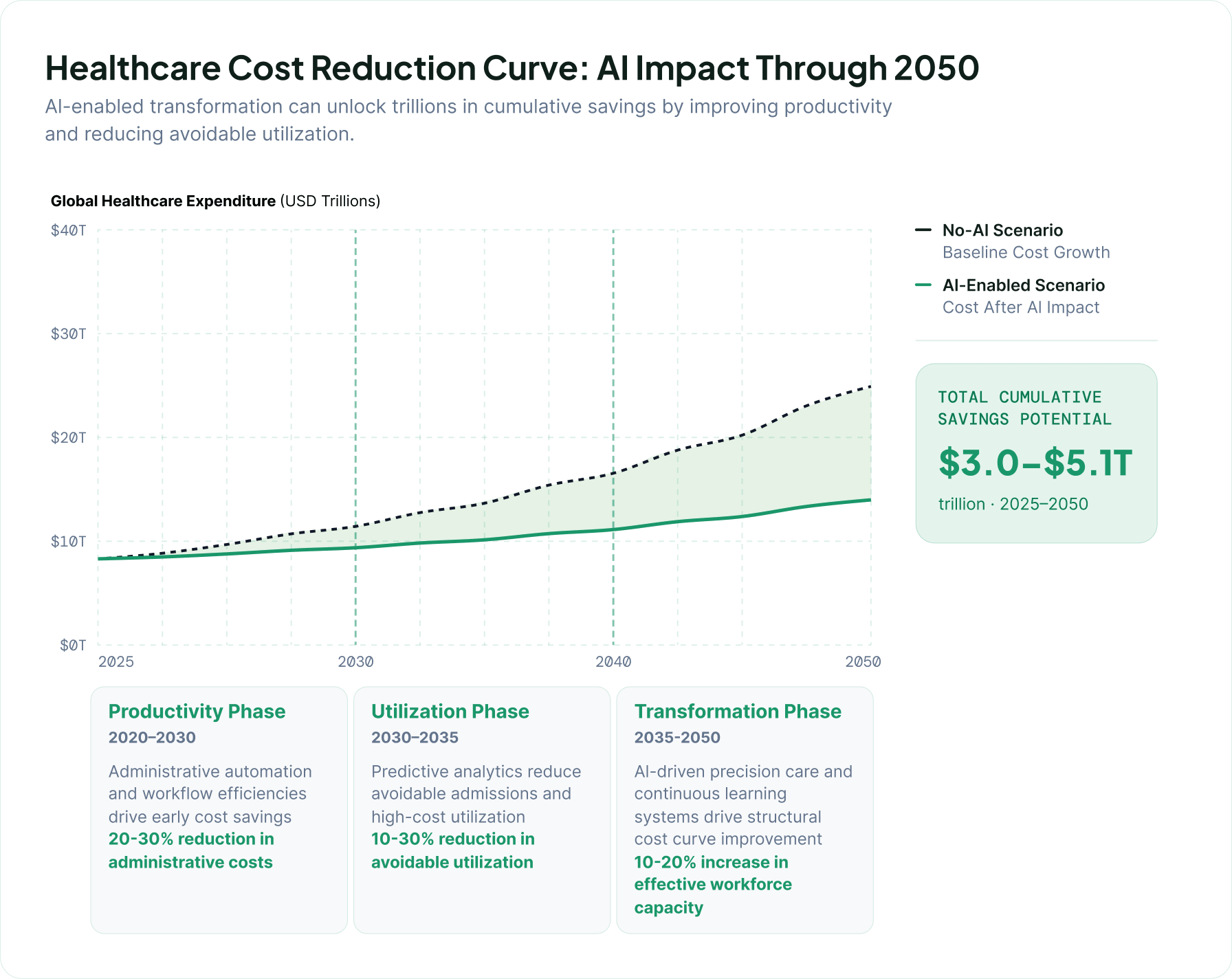

Cost savings and productivity gains represent the most immediate and measurable dimension of AI value in healthcare systems facing workforce shortages, demand growth, and administrative complexity. The core impact is concentrated in labor augmentation and efficiency improvements across clinical and operational workflows.

Morgan Stanley’s analysis highlights potential system-wide efficiency gains translating into trillions of dollars in cumulative savings by 2050 Morgan Stanley AI in Healthcare Insights. These projections reflect macroeconomic modeling of productivity improvements across global healthcare systems.

Industry estimates also project AI in healthcare reaching a $188 billion market by 2030, reflecting rapid adoption across diagnostics, administration, and clinical decision support.

Productivity gains are concentrated in three areas. Administrative automation reduces non-clinical workload. Clinical decision support improves throughput and reduces delays in diagnosis and treatment. Predictive analytics reduces downstream utilization through earlier intervention in high-risk patients.

Economic impact is driven by two mechanisms:

Realization of value depends on workflow redesign, data interoperability, and embedding AI outputs into operational decision pathways rather than standalone tools.

Over time, gains are expected to compound as AI shifts from discrete task automation toward integrated workflow optimization across the care continuum.

AI adoption is increasingly linked to revenue-generating care models as systems move beyond pilots toward scalable deployment. Continued venture investment of nearly $4B in healthcare AI reflects confidence in integrated delivery models rather than isolated tools.

Health systems are embedding AI into service lines such as triage, chronic disease management, and virtual care orchestration. These models shift AI from a supporting layer to a core component of care delivery.

AI diagnostics is emerging as a key revenue vector, with pricing models evolving toward per-study, per-member, or outcome-linked structures. Adoption depends heavily on workflow integration and reimbursement clarity.

Subscription and platform-based models are expanding, combining analytics, decision support, and care orchestration into unified offerings. These models align incentives with sustained outcomes and long-term engagement.

AI is increasingly a care model design decision rather than a procurement decision, with implications for both providers and payers in how services are structured and financed.

Measuring ROI remains a central challenge as healthcare AI moves into scaled deployment. Industry analyses emphasize that value realization requires multi-dimensional frameworks that extend beyond direct cost savings.

A common limitation is reliance on narrow financial metrics that overlook clinician time savings, quality improvements, and patient experience gains. Value is most accurately captured at the system level rather than individual tool level.

The most effective approaches combine these dimensions into continuously updated scorecards that track both operational and financial outcomes over time, enabling AI to be managed as an evolving capability rather than a static investment.

AI in healthcare is increasingly positioned as workforce augmentation rather than replacement, redistributing cognitive and administrative workload across clinical teams. The dominant pattern across physician and nursing contexts is capacity extension, reduced low-value task burden, and improved decision support, while preserving clinician judgment in care delivery.

Clinical perspectives highlight that AI is expected to support rather than replace diagnostic work, particularly in imaging-heavy specialties where workload pressure is high. This reflects a broader shift toward AI as a co-pilot embedded in clinical workflows rather than an autonomous decision-maker.

Workforce research from McKinsey indicates that clinicians show higher acceptance of AI when it reduces administrative burden and supports decision-making rather than replacing clinical judgment. Nurses in particular report stronger acceptance when AI is applied to documentation, coordination, and communication tasks.

AI is therefore reshaping task architecture rather than eliminating roles. Administrative and documentation tasks are the most readily automated. Diagnostic tools are most effective when positioned as second-reader or triage support. Workforce resistance is lowest when AI increases patient-facing time rather than reducing autonomy.

For healthcare executives, the strategic implication is that AI value should be measured as capacity expansion rather than headcount reduction. Organizations that position AI as workflow augmentation rather than cost-cutting replacement are more likely to achieve sustained adoption and productivity gains.

AI adoption is constrained less by model capability than by workforce readiness across clinical and administrative roles. Industry analysis from HIMSS emphasizes that successful adoption depends on organizational readiness, governance structures, and workforce AI literacy https://www.himss.org/resources.

For physicians and nurses, AI functions primarily as decision support and documentation assistance, reducing time spent on administrative tasks and enabling more patient-facing care. This shift requires training in interpreting AI outputs and understanding system limitations.

For administrative teams, AI accelerates automation in scheduling, revenue cycle management, and operational workflows, shifting roles toward oversight, exception handling, and process monitoring.

Three capability domains consistently determine adoption success:

KPMG highlights that AI integration fails when deployed without workflow redesign and structured change management.

Governance responsibility is increasingly distributed across IT, clinical leadership, and compliance functions rather than centralized in a single department. Continuous monitoring is replacing one-time validation as models evolve.

The primary constraint on scaling is workforce adaptability rather than technology availability.

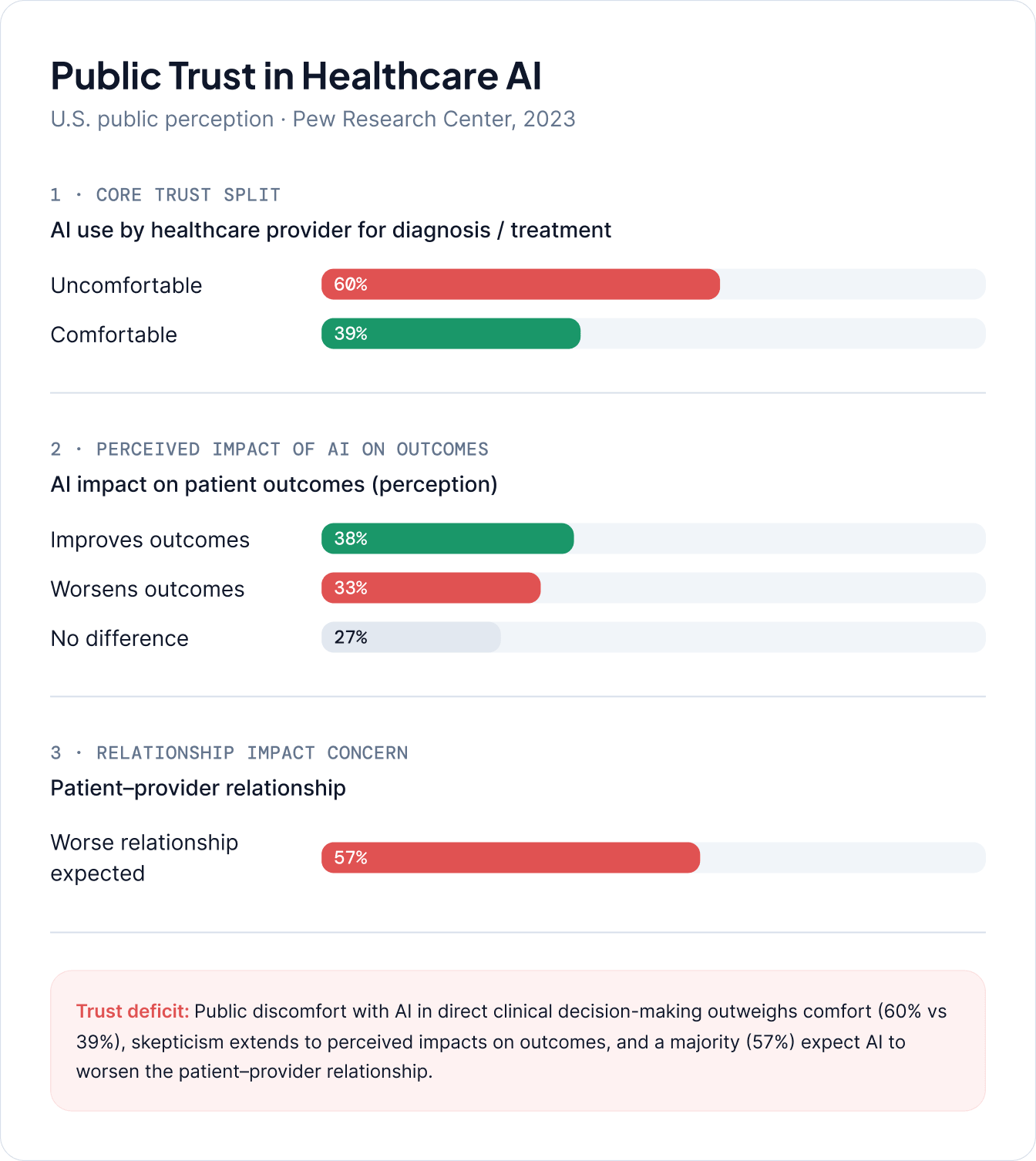

ç

Core trust concerns include:

For healthcare executives, trust must be treated as an operational requirement embedded in care design, not a communications function.

AI performance variability across patient populations remains a central clinical risk. Studies show that predictive models can underperform in specific demographic groups when training data is not representative.

The FDA classifies many healthcare AI systems as Software as a Medical Device (SaMD), requiring validation, lifecycle monitoring, and post-market surveillance.

Three primary reliability risks dominate:

Model reliability depends heavily on input data completeness and ongoing monitoring. Performance drift is a key operational risk as patient populations and workflows evolve.

AI governance must shift from static validation to continuous clinical monitoring with subgroup-level performance tracking.

Healthcare AI adoption progresses through four stages: experimentation, pilot deployment, enterprise integration, and AI-native operations. Industry frameworks such as HIMSS and Bessemer highlight this progression as both technical and organizational.

Experimentation involves isolated pilots in imaging, documentation, or administrative workflows with limited enterprise integration.

Pilot deployment introduces real-world testing within defined workflows such as radiology triage or revenue cycle optimization.

Enterprise integration embeds AI across service lines with governance, interoperability, and monitoring frameworks.

AI-native operations represent full integration where AI becomes a foundational layer of clinical and operational decision-making.

Progression depends more on organizational redesign than model adoption. The most difficult transition is from pilot to enterprise scale due to governance, infrastructure, and workflow integration requirements.

Scaling AI in healthcare is constrained primarily by structural and operational factors rather than model capability. As industry analyses from McKinsey and KPMG highlight persistent barriers across systems.

Data fragmentation across EHRs and legacy systems limits model performance and generalizability. Workflow integration challenges prevent seamless embedding of AI into clinical practice.

Procurement processes are often misaligned with iterative AI development cycles, slowing deployment. Clinician trust and concerns about transparency also limit adoption.

Cybersecurity and data governance requirements add additional constraints as AI systems expand access to sensitive data.

Successful scaling depends on simultaneous investment in data infrastructure, workflow redesign, and governance maturity.

Successful AI adoption requires structured deployment rather than ad hoc experimentation. Industry guidance from Deloitte and KPMG emphasizes phased implementation aligned with governance maturity and workforce readiness.

Phased deployment begins with high-value, well-defined use cases where workflow boundaries are clear and measurable outcomes can be tracked.

Governance evolves from innovation teams to cross-functional structures involving clinical leadership, IT, compliance, and risk management. Continuous oversight replaces one-time approval.

Vendor selection increasingly prioritizes interoperability, integration capability, and lifecycle support rather than standalone functionality.

Pilot evaluation must include workflow impact, clinician adoption, and operational performance, not only technical accuracy.

Enterprise scaling requires standardized infrastructure, centralized monitoring, and workflow redesign to embed AI into care delivery systems.

Key best practices include:

Healthcare AI is evolving toward multimodal, agentic, and ambient systems that integrate data and automate workflows across clinical environments. Industry analysis highlights a shift from standalone tools to integrated operational systems.

Multimodal AI integrates imaging, clinical notes, genomics, and physiological data into unified models for more context-aware decision support.

Agentic systems extend AI from decision support to workflow orchestration, enabling automated task sequencing and escalation.

Ambient intelligence reduces clinician burden through passive data capture and continuous monitoring embedded in clinical environments.

Autonomous operations are emerging in non-clinical domains such as scheduling and revenue cycle management, though clinical autonomy remains limited due to regulatory and safety constraints.

Digital twins enable simulation of patients, workflows, and hospital systems for predictive planning and optimization.

Healthcare AI adoption will diverge across systems depending on infrastructure maturity, regulation, and organizational transformation capacity. Industry forecasts suggest varying levels of system-wide impact.

In the conservative scenario, AI remains primarily a supporting layer for documentation, diagnostics, and administrative optimization without major structural change.

In the accelerated transformation scenario, AI becomes embedded in workflows, enabling redesigned care pathways and integrated decision support systems.

In the AI-native scenario, healthcare systems operate as continuously optimized networks where AI drives clinical, operational, and financial decision-making.

Transformation is driven more by system redesign than by algorithmic capability alone.

AI adoption is shifting from experimentation to measurable operational and financial impact, with implications varying across stakeholders.

For hospital systems, priorities include workflow integration, governance maturity, and measurable productivity gains.

For insurers, AI is increasingly central to risk stratification, claims automation, and care management optimization.

For investors, differentiation depends on scalable integration, interoperability, and demonstrated clinical adoption rather than experimental tools.

For policymakers, regulatory clarity around accountability, safety, and data governance is essential for scaling adoption.

Clinicians experience AI primarily as workflow augmentation, with adoption driven by trust, usability, and reduction of cognitive burden.

For technology vendors, competitive advantage increasingly depends on interoperability, integration depth, and measurable outcomes rather than model capability alone.

AI adoption in healthcare is accelerating due to sustained pressure on health systems to improve productivity, address workforce shortages, and manage rising clinical and administrative complexity. Across diagnostics, administration, predictive care, and precision medicine, AI is increasingly embedded into core workflows rather than remaining a peripheral innovation layer. Companies like CleverDev Software are helping healthcare organizations operationalize this shift by developing scalable AI-driven solutions tailored to clinical and enterprise environments. This transformation is reinforced by industry analysis showing rapid movement from experimentation toward scaled deployment and enterprise integration.

The most immediate and measurable value from AI is emerging in administrative automation, clinical documentation, revenue cycle optimization, and diagnostic support. These areas consistently demonstrateproductivity gains through reduced manual workload, improved throughput, and enhanced decision support. Over time, additional value is expected from predictive analytics, population health management, and precision medicine applications that enable earlier intervention and more individualized care delivery. KPMG highlights that the largest gains occur when AI is embedded into workflows rather than deployed as standalone tools. This is where technology partners such as CleverDev Software play a critical role by integrating AI capabilities into existing healthcare ecosystems without disrupting clinical operations.

Realizing this value depends on three core implementation priorities. First, health systems must invest in data infrastructure and interoperability to ensure AI systems can operate on complete and high-quality clinical information. Second, workflow redesign is essential so that AI outputs are integrated into clinical and operational decision pathways rather than added as separate tools. Third, governance maturity must evolve to include continuous monitoring, bias detection, and clear accountability structures across clinical, operational, and IT domains.

At CleverDev Software, we are confirmed that over the long term, AI is expected to shift healthcare from episodic, reactive care delivery toward continuously optimized, data-driven systems. This includes the gradual emergence of AI-enabled operating models where administrative processes are increasingly automated, clinical decision support is embedded in real time, and care pathways are dynamically adjusted based on predictive insights. However, this transformation is dependent on sustained progress in trust, regulation, and system-level integration, not solely on advances in model capability.